Inheritance tax is a tax on property inherited when a parent or relative dies. Inheritance tax is an important issue for those who receive an inheritance. However, there are many points that are difficult for many people to understand and need to know, such as how the tax is actually levied, how much property is subject to tax, and the scope of the basic exemption. In this article,An administrative scrivener qualified as an advanced inheritance diagnosticianThis section provides basic knowledge of inheritance taxes in an easy-to-understand manner and introduces important points to keep in mind when inheriting an estate. Proper preparation will help you prepare for future inheritances.

Inheritance Tax Calculation Flow

Inheritance tax is one of the most important procedures that cannot be avoided when inheriting an estate. However, its calculation is complex and often confusing to many people. First, we will explain the basic process of calculating inheritance tax.

The "original inheritance" and the "deemed inheritance" left by the decedent (the deceased) are totaled, and the "tax-exempt property" is subtracted from this amount.

What is a taxable inheritance? Calculation of Taxable Value

Not all property is subject to inheritance tax.Certain assets may be treated as tax exempt, reducing the burden for heirs.For example, property that meets certain conditions, such as life insurance proceeds, condolence money, cemeteries, and headstones, is exempt from inheritance tax. Knowing more about these assets will help make the inheritance process go more smoothly.

What is included in the inheritance

Original inheritance

Property acquired by inheritance, etc. in accordance with the provisions of the Civil Code is referred to as "original inherited property.

- Land, buildings, savings, securities, golf club memberships, jewelry and other precious metals, antiques, loans, copyrights, and other items that can be estimated in monetary termsAnything with economic value is inherited propertyThe first two are the following.

- The economic value of the portion of a life insurance policy that has not yet resulted in an insured event at the time of inheritance (excluding policies that do not pay a cash surrender value, etc.) and that corresponds to the premiums paid by the decedent (the right to receive a cash surrender value, etc.) is called "rights related to life insurance policies,Contracts in which the contractor is the decedent are inherently inherited property.(Handling of the following insurance policies (1))

deemed inheritance

In order to ensure fairness in taxation, the following items, which are not inherited property under the Civil Code but have substantially the same effect as inherited property, are included in taxable property as "deemed inherited property" under the Tax Law.

However, it is not an inheritance under the Civil Code,It is not included in the property to be divided.

- death benefit

Of the death benefit received upon the decedent's death, the portion of the death benefit equivalent to the premiums paid by the decedent is deemed to be the deemed inherited property. (Treatment (2) for the following insurance policies) - death benefit

Retirement benefits received as a result of the decedent's death and confirmed within three years of the decedent's death are deemed inherited property and subject to inheritance tax. - Life Insurance Rights(Treatment of insurance policies below (iii))

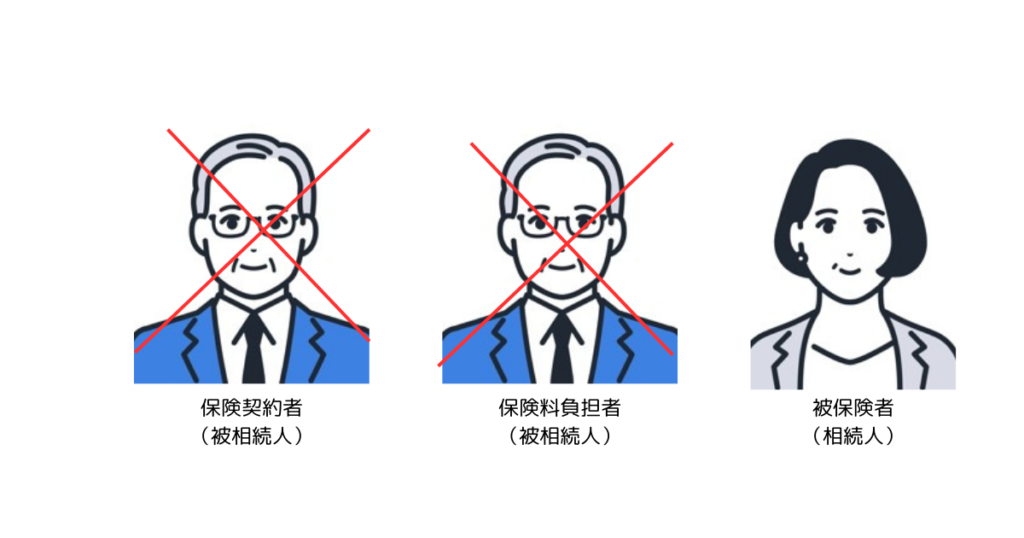

Note that insurance contracts are handled differently depending on who is the policyholder (the person entitled to receive insurance benefits), who is the premium payer (the person paying the premiums), and who is the insured (the person covered by the insurance contract).

Case 1: The amount equivalent to the surrender value is the "original inheritance".

For an insurance policy in which the decedent (deceased father) is the policyholder (beneficiary) and at the same time bears the premiums, if the insured (person covered by the insurance policy) is other than the decedent (mother), no insurance benefits are paid while the mother is alive, but the amount equivalent to the surrender value becomes the "original inheritance".

Case 2: Of the death benefit received, the portion corresponding to the premiums paid by the decedent is deemed inherited property.

If the policyholder (beneficiary) is a person other than the decedent (child) and the decedent (deceased father) is the insured (person covered by the insurance policy) and the death benefit is paid, the portion of the death benefit equivalent to the premiums paid by the decedent is a deemed inheritance property and subject to inheritance tax.

In this case, the insurance proceeds paid become the unique property of the child who is the policyholder (beneficiary of the insurance proceeds), and are therefore subject to inheritance tax but not to division of the estate.

Case 3: The amount equivalent to the surrender value is "deemed inherited property.

If the policyholder is a person other than the decedent (child), the decedent (deceased father) is the premium payer, and the insured is a person other than the decedent (mother), the insurance benefit is not paid while the mother is alive, but the amount equivalent to the surrender value is deemed to be inherited property.

As in Case 1), it is the "amount equivalent to the surrender value" that is considered to be the inherited property, whereas Case 1) is the subject of the "estate division agreement" as the original inherited property,This case is not subject to "estate planning".

Deductions from the estate

liabilities

Debts (e.g., debts) belonging to the decedent's burden can be deducted from the inheritance as a negative legacy if their amount is fixed at the time of inheritance.

However, only those inherited by the heirs and comprehensive devisees (those who were given the right to inherit a certain percentage or part of the entire inheritance comprehensively, rather than a specific property by will), and those who have renounced their inheritance or lost their right to inherit (disinherited) cannot deduct the debt.

- Deductible items

- loan payable

- unpaid medical expenses

- Unpaid income, inhabitant, and property taxes on the decedent

- Items that cannot be deducted

- Accounts payable for purchase of cemetery

- Guaranteed debt (deductible when debtor is insolvent)

- Loan with group credit life insurance

- Probate expenses

- Attorney fees, tax accountant fees, judicial scrivener fees, administrative scrivener fees

funeral expenses

- Deductible items

- wake expenses

- Funeral expenses, offerings, and payment of burial expenses

- Expenses incurred before or after the funeral that are considered normal and necessary

- Search and transport costs for dead bodies

- Items that cannot be deducted

- Koso Return Expense

- Buddhist memorial service expenses

- Autopsy fees

Cemeteries, Buddhist altars, and Buddhist altar and utensils (for daily worship)

This may seem a bit complicated and confusing with the cemetery borrowing accrual mentioned in the "non-deductible items" section above. Cemeteries and headstones purchased by the decedent (the deceased) during his/her lifetime are not taxed as inherited property. However, the unpaid amount owed for the purchase of the cemetery, which has not yet been paid, is not exempt from estate tax, but the unpaid amount may be deductible as a debt.

- Tax Exemption

This refers to property that is not subject to inheritance tax in the first place. For example, cemeteries, headstones, and Buddhist altars are not subject to inheritance tax.tax-exempt propertyare. These assets are excluded from estate taxation and their value is not included in the estate for purposes of reporting and taxation. In other words, these are items that do not have to be included in the calculation as inherited property.Example: Cemeteries and headstones purchased by the decedent during his or her lifetime are exempt from taxation, so their value is not included in the estate's estate taxable estate. - debt forgiveness

On the other hand,debt forgivenessis a mechanism that allows debts, such as debts and accrued liabilities owed by the decedent at the time of death, to be deducted from the total inheritance. Inheritance tax is basically calculated based on the total value of the estate, but by subtracting the amount of the decedent's debts, if any, the amount of the estate subject to taxation is reduced.

ExampleThe following is an example: if the decedent did not pay for the purchase of the cemetery before his/her death and there is a remaining payment (unpaid), the unpaid amount can be deducted from the total inheritance as a "debt", which may result in a lower inheritance tax liability. - Point of Difference

tax-exempt property: not included in the inheritance and not taxed in the first place.

debt forgiveness: The taxable amount is reduced by subtracting it as a liability from the total inherited property.

Thus, the cemetery itself is not taxable, but the accrued amount has the effect of reducing the taxable estate as a debt deduction.

Certain amount of death benefit

Considering that life insurance proceeds are a living security for the surviving family members, the death benefit received by the heirs is exempt from taxation up to the amount calculated according to the following formula.

Exemption limit = 5 million yen x number of legal heirs

As mentioned above, life insurance proceeds are regarded as the unique inheritance of the insurance beneficiary and are not subject to division of the estate. If multiple heirs receive life insurance proceeds, the tax exemption amount applicable to each heir is calculated by dividing the maximum tax exemption amount calculated above proportionally among the heirs who actually received the insurance proceeds, based on the ratio of the amount of insurance proceeds they acquired.

Certain amount of death benefit

Death benefits received by heirs are exempt from taxation up to the amount calculated by the following formula, for the same purpose as life insurance.

Exemption limit = 5 million yen x number of legal heirs

As with life insurance, the calculation of the tax-exempt amount and the number of legal heirs in the case where multiple heirs receive the death benefit will be prorated based on the percentage of the amount of the death benefit acquired among the heirs who actually received the death benefit.

The "number of legal heirs" under the Inheritance Tax Law is subject to two modifications to the "number of legal heirs under the Civil Code".

This is a measure to maintain fairness in inheritance tax, since the number of legal heirs is used in the calculation of inheritance tax deductions under the tax law.

For example, as shown below, there is no limit under the Civil Code on the number of adopted children, but there is a limit under tax law.

It prevents the number of adopted children from increasing to five or six in order to avoid the imposition of inheritance taxes.

- Limitations on the number of adopted children

The number of adopted children that can be included in the legal heirs for the purposes of calculating the "basic allowance for the estate," "total inheritance tax," and "maximum exemption amount for death benefits and death benefits" under the inheritance tax is limited as follows.

If the heir has a biological child - 1

If there are no biological children among the heirs: 2

However, the following persons are considered biological children and are not subject to the limitation on the number of adopted children- Special adoptions (see separate column)

- A spouse's biological child (stepchild) who was adopted by the decedent

- A person adopted by a spouse by special adoption who is the adopted child of the decedent

- Assumed heirs such as biological or adopted children (see separate column)

- If there is a waiver of inheritance

Under the Inheritance Tax Law, even if there is a waiver of inheritance, the legal heirs are assumed as if there was no waiver, and the "basic exemption amount for the estate," "total inheritance tax," "maximum exemption amount for death insurance benefits and death benefits," and "reduced tax rate for spouses" are calculated based on the assumed number of legal heirs.

Like the limitation on the number of adopted children, this system prevents the reduction of inheritance taxes by arbitrarily (deliberately) increasing the number of heirs by renouncing inheritance.

For example, if the heirs are a spouse and one child, the decedent's parents have already died, and the decedent has five siblings, the original heirs are the spouse and one child, but if the child renounces the inheritance, the total number of heirs becomes six, including the spouse and five siblings, and the basic exemption amount increases, resulting in lower inheritance taxes. To prevent this, the tax law calculates inheritance tax assuming the child as an heir even if the child renounces inheritance.

Condolence money, etc.

Condolence money," "wreath money," "funeral expenses," etc. received by the heirs, etc. from the company for which the decedent worked upon the decedent's death are exempt from taxation up to the amount calculated as follows, except for those that are deemed to be death benefits in substance. The portion exceeding this amount will be treated as "death benefits.

In case of death in the line of duty

Decedent's regular salary at the time of death x 36 months

In case of death outside of work

Decedent's regular salary at the time of death x 6 months

Property that meets certain requirements when donated to national and local governments

If a person who has acquired property by inheritance or bequest donates inherited property that meets certain requirements to the national government, a local government, or a specific public benefit corporation by the deadline for filing inheritance tax returns, the donated property is exempt from taxation.

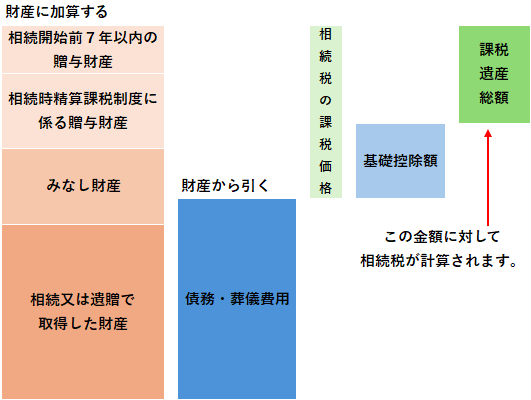

Items to be added to the estate

Amount of gift under the taxation system for settlement at the time of inheritance

Amount of gift within 7 years before the start of inheritance (revised in 2024)

Amount of gift within 7 years prior to commencement of inheritance

What is the amount of property subject to inheritance tax and the total taxable estate?

The "taxable gross estate," an important concept when calculating inheritance tax, is the "taxable value" calculated based on the above calculations minus the "basic deduction" described below, which is the basis for the amount actually taxed on the estate received by the heirs.This amount will ultimately be subject to inheritance tax.

Basic deduction for legacy

30 million yen + 6 million yen x number of legal heirs

Total taxable estate

Taxable value - Basic deduction for the estate

Total amount of inheritance tax and the amount of inheritance tax for each heir

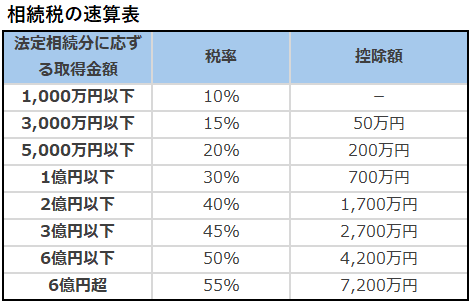

Find the total amount of inheritance tax

The "total amount of inheritance tax."The total amount of inheritance tax for all heirs on the total taxable estate.

The total amount of the taxable estate.Assuming that the legal heirs have divided the property according to the legal share.The amount of property to be acquired by each heir is calculated, and the total tax amount is calculated by multiplying each property amount by the progressive inheritance tax rate.

The calculation for this total amount is,The "total inheritance tax" is determined regardless of who actually inherits how much.

(Example.)

If the legal heirs are the wife, the eldest son, and the two eldest daughters, and the "total taxable estate" calculated above is 120 million yen

The property acquired by each of the legal heirs is

Wife: 1/2 = 60 million yen

Eldest son: 1/2 x 1/2 = 1/4 = 30 million yen

Eldest daughter: 1/2 x 1/2 = 1/4 = 30 million yen

The amount of inheritance tax on the above-mentioned acquired property is calculated according to the following "Inheritance Tax Quick Calculation Table".

Wife: 60 million yen x 30% - 7 million yen = 11 million yen

Eldest son: 30 million yen x 15% - 500,000 yen = 4 million yen

Eldest daughter: 30 million yen x 15% - 500,000 yen = 4 million yen

The total amount of inheritance tax is as follows

11 million yen + 4 million yen + 4 million yen = 19 million yen

Determine the taxable value of each person based on the division of the estate

In many cases, the division of an estate does not always follow the legal inheritance division.

For example, there are cases in which the inheritance is not divided in accordance with the legal inheritance shares because the method of dividing the estate was specified in the will, or because land is included in the inheritance and is difficult to divide.

The "percentage of taxable value" is calculated based on the taxable value of each heir after subtracting each heir's non-taxable assets and debts inherited by each heir and funeral expenses, etc. incurred by each heir from the amount of property acquired by each heir as determined through estate division discussions, etc.

In this case, the taxable value on which the calculation is based is "the total taxable value before subtracting the basic allowance.

(Example.)

In the above example, if the division of the estate is as follows: Wife: JPY180,000,000, eldest son: JPY33,600,000,000, and eldest daughter: JPY33,600,000,000.

Each person's share of the inheritance is

Wife: ¥100,800,000 ÷ ¥168,000,000 = 60%.

Eldest son: 33.6 million yen ÷ 168 million yen = 20%.

Eldest daughter: 33.6 million yen ÷ 168 million yen = 20%.

Calculate the amount of inheritance tax for each person based on the percentage of inheritance for each person

(Example.)

Wife: 1.9 million yen x 60% = 11.4 million yen

Eldest son: 1.9 million yen x 20% = 3.8 million yen

Eldest daughter: 1.9 million yen x 20% = 3.8 million yen

Calculate the amount of tax due for each person under the various systems

Based on the amount of inheritance tax for each person calculated above, various systems are available to take into account each person's circumstances.

The actual amount of tax due is determined by applying these systems.

- 20% additional

Spouse and children of the decedent (including grandchildren, etc., who became heirs by descent), and parents.If a person who is a "qualified person" acquires property by inheritance or bequest, the amount of inheritance tax payable by that person is the amount of the calculated inheritance tax on that person, plus 20%. In other words, the tax amount is increased by 20%. - tax deduction for a donation

If a person who has acquired property by inheritance or bequest has acquired property from the decedent by gift within 7 years before the start of inheritance (with the 2024 amendment and special provisions), then, in accordance with the provisions of the "additional gift before death," theInheritance tax is calculated by including the donated property in the estate.

However, if gift tax is paid at the time of the gift, the gift tax paid at the time of the gift is deducted from the inheritance tax, since this would result in double taxation of inheritance tax and gift tax. - Tax Reduction for Spouses

Spouses are entitled to reduced inheritance taxes in consideration of their contribution to the decedent's estate. This treatment applies to the spouse who is the spouse on the family register at the time of inheritance, regardless of the length of the marriage. It does not apply to those who are de facto married, such as common-law wives.

By this system,There is no inheritance tax on the spouse up to the total taxable value of 160 million yen or the legal inheritance share, whichever is greater.

Please refer to the other column for the application of this system, as there are some points to be noted. - tax exemption for minors

In consideration of the burden of childcare expenses until the heir reaches the age of majority, if a minor who satisfies all of the following requirements inherits property, an amount equal to 100,000 yen per year for the period from the age at which the inheritance begins until the minor reaches 18 years of age may be deducted from the calculated inheritance tax. Furthermore, if the amount of deduction for a minor exceeds the amount of inheritance tax for that person, it can be deducted from the amount of inheritance tax for the person responsible for his/her support (mother, etc.).- Be an unlimited taxpayer (see separate column)

- Must be a legal heir

- Acquisition of property by inheritance or bequest.

Deduction for minors = 100,000 yen x (age 18 - age at start of inheritance)

- tax exemption for the handicapped

If a disabled person who meets all of the following requirements acquires property, an amount equal to 100,000 yen per year (200,000 yen in the case of a person with special disabilities) multiplied by his/her age at the start of inheritance until he/she reaches 85 years of age may be deducted from the calculated inheritance tax amount. Furthermore, if the amount of the disability exemption exceeds the amount of the person's inheritance tax, it can be deducted from the amount of inheritance tax of the person responsible for his/her dependents.- Be a resident unlimited taxpayer (see separate column)

- Must be a legal heir

- Acquisition of property by inheritance or bequest.

Disability exemption = ¥100,000 (or ¥200,000) x (age 85 - age at start of inheritance)

- multiple inheritance exemption

When successive inheritances occur, the taxpayer is again subject to inheritance tax on the same property, which places a heavy burden on the taxpayer. Therefore, if inheritance tax is imposed again within 10 years, a certain amount of the tax imposed on the previous inheritance can be deducted from the amount of inheritance tax to be imposed on the subsequent inheritance. - foreign tax amount reduction

This system is designed to adjust for international double taxation when foreign property is acquired through inheritance or bequest and foreign inheritance tax is imposed on the property.

As a result, in the above example, if there are no special circumstances for the two children to be exempted, the wife's inheritance tax will be reduced by the "spouse's tax reduction" and no inheritance tax will be due, and the inheritance tax payable will be 7.6 million yen for the two children.

summary

How was it?

The inheritance tax system and calculations are very complex and there are many aspects that are difficult to understand.

However,Inheritance tax returns are due within 10 months from the day following the day on which the taxpayer became aware of the inheritance.Since delinquent taxes and additional taxes may be imposed if the filing deadline is missed, it is necessary to proceed with the necessary procedures as soon as possible.

Instead of panicking after an inheritance has been received, it is recommended that measures be taken in advance with the help of experts based on the above knowledge.

Comments