Regardless of the variety of inherited assets, it is very important to "think about inheritance in advance.

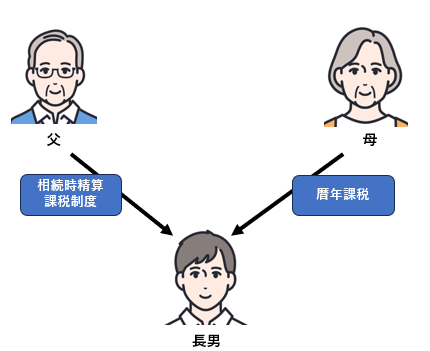

Inheritance tax can be reduced by gifting a portion of one's property to one's children or grandchildren during one's lifetime and passing the property on to the next generation in advance. Typical and well-known methods of transferring assets areThere are two types of taxation systems: the calendar year taxation system and the taxation system for taxable income at the time of inheritance.The calendar year taxation system isUp to 1.1 million yen tax-free each yearThis is a good way to prevent inheritance tax. By gifting assets to your children and grandchildren in increments of 1.1 million yen each year, you can transfer assets to your children without paying gift taxes and reduce your own estate, thereby preventing inheritance taxes.

taxation system allowing for settlement at the time of inheritanceis a system that allows one donor (the person giving the gift) to receive a gift of up to a cumulative total of 25 million yen for one donee (the person receiving the gift) without paying gift tax.

Transfer your property to your children and grandchildren while you are alive today,Living Gifts."One of the ways of"Inheritance Settlement Tax System."This section describes the following

This article is intended to provide an introduction to the general basics of inheritance tax.

Consult a tax attorney for individualized and specific inheritance tax advice and calculations.

Inheritance tax measures (2) - Inheritance taxation system

Features of the Inheritance Taxation System

The taxation system for taxable assets at the time of inheritance is a system that encourages the transfer of assets (gifts during one's lifetime) from parents or grandparents to children or grandchildren.

No gift tax is imposed up to a cumulative total of 25 million yen.

However, it should be noted that property (up to a cumulative total of 25 million yen) that was gifted using the taxation system for settlement at the time of inheritance,Become an inheritance subject to inheritance tax when an inheritance occurs.This means that when the donor dies, the inheritance tax is paid in a lump sum. In other words, when the donor dies, the inheritance is calculated from the sum of the value of the donated property and the value of the inherited property, and a lump-sum inheritance tax is paid.

That is, for those who have a lot of land and other real estate and financial assets,You will pay estate tax at a higher rate than gift taxTherefore, there is no advantage to using this system.

Conversely, for those who "have little or no inheritance" or "have no inheritance tax because of debts," this system allows them to use the system,You may be able to transfer property to your children or grandchildren without paying either gift or estate taxes.

2024 revision

In addition to the special deduction of ¥25 million accumulated to date, gifts of ¥1.1 million or less per year are now exempt from taxation. The basic exemption of 1.1 million yen per year is not included in the special exemption (cumulative total of 25 million yen) and is not added to the inheritance at the time of inheritance. In other words, the 2024 amendment has increased the benefits of the "taxation system for settlement at the time of inheritance. The following is an example of a calculation of the maximum amount that is not subject to gift tax.

25 million yen (cumulative) + 1.1 million yen x number of years donated

If the above amount exceeds 25 million yen,A 20% gift tax is imposed on the amount in excess.However, the gift tax paid will be deducted when calculating inheritance tax at the time of inheritance.

In addition, under this amendment, if the calendar year taxation system is used instead of the taxation system for the settlement taxation at the time of inheritance, gifts made within seven years of the year of death will be added to the inheritance as if the gifts had never been made. (For more information, please seeCalendar Year Taxation System Columnfor more information).

Specific examples of the taxation system for settlement at the time of inheritance

Let us now take a look at the Inheritance Settlement Tax System with some specific examples.

Difference by the amount of inherited property

First, there is a difference between having property subject to inheritance tax and not having property subject to inheritance tax.

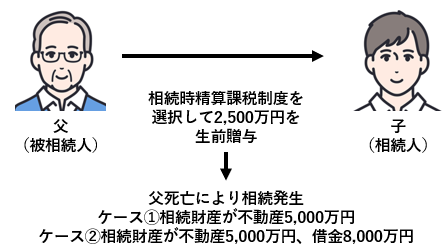

The 25 million yen donated during one's lifetime by electing the taxation system for settlement at the time of inheritance will be added to one's inheritance and subject to inheritance tax.

Case (1)

The total taxable value of the inheritance is 75 million yen, which is the sum of 50 million yen of inherited property and 25 million yen for which the taxation system for the settlement of taxation at the time of inheritance is selected,Inheritance tax amount is 5.8 million yenThe first two are the following.

75 million yen - 36 million yen (basic deduction) = 39 million yen x 20% - 2 million yen = 5.8 million yen

Case (2)

The inheritance taxable value is 75 million yen, which is the sum of 50 million yen of inherited property and 25 million yen from the taxation system for taxable settlement at the time of inheritance. However, if there are debts of 80 million yen at the time of inheritance, these debts will be deducted from the taxable amount of inheritance tax,No inheritance tax.

A bit of an extreme example.

My own experience was case (2).

I had not prepared any inheritance tax plan, and in my grief and confusion over the loss of my mother, I consulted an administrative scrivener and a tax accountant and proceeded with the inheritance procedures. I remember that I panicked.

Afterwards, when we proceeded to liquidate the estate, we discovered that there was no inheritance tax due on the remaining debt for the construction costs of the real estate.

If we had not had the debt, we would have had to sell some of our inherited real estate to pay the estate taxes. We realized that we needed to take action as soon as possible.

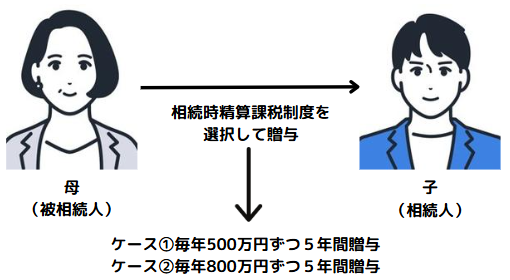

Differences by amount of donated property

Case (1)

(5 million yen - 1.1 million yen) x 5 years = 19.5 million yen <25 million yen

In this case, the gift is below the 25 million yen basic exemption,No gift tax is due.

However, if the mother passes away and the inherited assets are 50 million yen, the 19.5 million yen that was exempted from inheritance tax is added to the inherited assets, and the inherited assets are 69.5 million yen.Subject to inheritance tax.

Case (2)

(8 million yen - 1.1 million yen) x 5 years = 34.5 million yen > 25 million yen

In this case, it is because the gift exceeds the basic exemption of 25 million yen,A gift tax of 20% = 1.9 million yen will be imposed on the 9.5 million yen (34.5 million yen minus the 25 million yen basic deduction).

In this case, the 1.9 million yen in gift tax paid is deducted from the inheritance tax.

Persons to whom the taxation system for taxation on settlement at the time of inheritance is applied

There are restrictions on the donor (the person giving the money) and the donee (the person receiving the money) for gifts that are eligible for the taxation system for settlement at the time of inheritance. Gifts from persons other than those listed below, or gifts received by persons other than those listed below, are not eligible for this system and are subject to gift tax.

It is important to note that this system cannot be used in the case of a gift to a spouse or to a brother who is another presumed heir because he has neither spouse nor children.

- Donor: Parents or grandparents age 60 or older

- Beneficiary: Child or grandchild over 18 years of age

Note that children must be presumed heirs (including heirs by descent) and grandchildren need not be presumed heirs.

This is not surprising, since grandchildren are not presumed heirs unless the child is deceased.

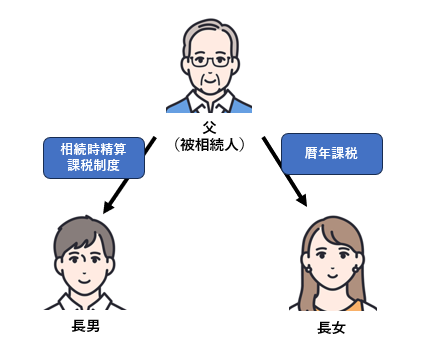

Relationship between the taxation system for settlement at the time of inheritance and calendar year taxation

As discussed in the Gift Tax column, calendar-year taxable gifts (tax-exempt up to ¥1.1 million per year) and the taxable settlement at the time of inheritance system are elective.

And this choice,Can be selected per donor or per doneeThe following is a list of the most common problems with the

However,Once the inheritance taxation system is selected (by filing a notification with the tax office), gifts made in subsequent years will automatically be subject to the inheritance taxation system and cannot be changed back to the calendar year taxation system.

To summarize the relationship between the taxation system for settlement at the time of inheritance and calendar year taxation

- Optional for each donor and donee

- Once a taxpayer selects the taxation system for inheritance at the time of inheritance, it cannot be changed during the lifetime of the taxpayer.

- Up to 25 million yen in cumulative total if you choose the taxation system for settlement at the time of inheritance

Each donee (recipient of property) can choose separately whether to elect the taxation system of the settlement taxation at the time of inheritance or the calendar year taxation.

Conversely, for each donor (the person who transfers property), the donee (the person who receives property) can separately choose whether to elect the taxation system of taxation on settlement at the time of inheritance or the calendar year taxation.

Points to note about the taxation system for taxation on settlement at the time of inheritance

The 2024 amendment has made the taxation system easier to use, but as mentioned above, there are some points to note. There are advantages and disadvantages to this system.

Gifts of up to ¥1.1 million per year do not count toward the ¥25 million limit of the taxation system for taxable income at the time of inheritance.

Each donor can choose whether to be taxed under the taxation system for settlement at the time of inheritance or calendar year taxation.

No gift tax is imposed on gifts up to a cumulative total of ¥25 million, whether given as a single gift or divided into multiple gifts.

There are no restrictions on assets to be donated under the taxation system for settlement taxation at the time of inheritance. Both cash and real estate are possible.

Once a person chooses the taxation system for the settlement taxation at the time of inheritance, he/she cannot return to the calendar year taxation system.

I cannot use the special exception for small residential lots. (For more information on special exceptions for small residential lots, please click here.)

The above is an introduction to the Inheritance Settlement Taxation System.

The Japanese government has established various systems for inheritance and gifts to protect the lives of its citizens. Please consider making good use of these systems as a way to pass on your valuable assets to your loved ones.

Comments