What is the 20 million yen retirement age problem?

First, let's look back at the "20 Million Yen Issue" referred to in the report "Asset Formation and Management in an Aging Society" submitted by the Market Working Group of the Financial Services Agency's Financial System Council on June 3, 2019.

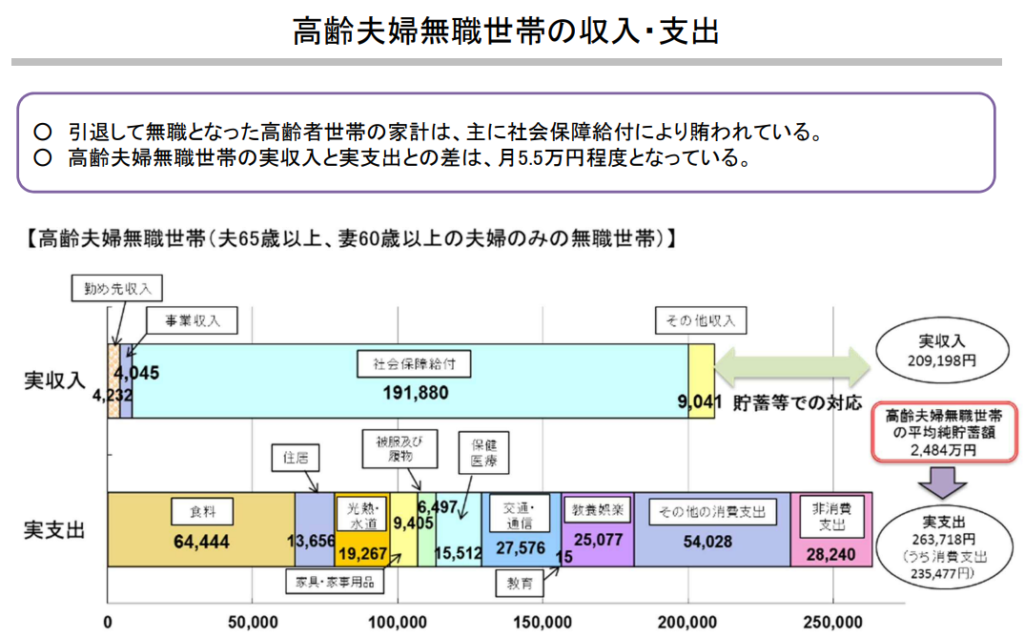

Based on the average household income and expenditure of an elderly couple unemployed household, the report shows that the average expenditure is 263,718 yen compared to an average income of 209,198 yen. According to this calculation, a monthly shortfall of 54,506 yen, or about 654,000 yen per year, is reported.

And if retirement is calculated as 30 years from the age of 65, it was reported that there would be a shortfall of approximately 20 million yen.

(Source:Ministry of Internal Affairs and Communications, "Household Survey" (2017))

This report has become a hot topic, and many of you may have felt the need to save to prepare for retirement.

The Japanese Economy Starting to Change: The 40 Million Yen Problem in Old Age?

Five years after the "20 million yen for retirement" issue announced in 2019, the Japanese economy is now in the midst of a major transformation. Until now, since the bursting of the bubble economy in the late 1990s, Japan's economy has been in a period of super-deflation, known as the lost 30 years.

In a deflationary world, prices of goods were falling rapidly, and payroll income tended to fall rather than maintain itself. As prices stagnated, companies were forced to perform poorly, and stock prices continued to slump.

In such a world, saving money and saving for retirement was a meaningful action.

Deposits are limited to 10 million yen per depositor per financial institution, up to the principal amount of 10 million yen and interest on the principal amount.deposit protection systemThe "I" is protected by the "I". Now let's take a look at thisIs there no risk in savings accounts?

In May 2024, Japan saw a y/y price increase of 2.81 TP3T, according to the Ministry of Internal Affairs and Communications.

(Source:Consumer Price Index 2020, Statistics Bureau, Ministry of Internal Affairs and Communications)

I am sure that all of you are aware of the rapid increase in the prices of things in your daily lives.

The price of a beef bowl has increased from 290 yen as of March 2018 to 400 yen as of July 2023. In about 5 years, the price will increase by about 1.4 times (140%). On the other hand, wages at major companies have barely increased by 51 TP3T in this year's Spring Struggle.

What this fact means is that now10 million yen deposited in the bank in 10 years.The face value remains the same at 10 million yen, but assuming that prices continue to rise at 2.51 TP3T per year, theReal value drops to 7.81 million yen.After 20 years, it will be a whopping 6.1 million yen.

In other words, if prices continue to rise at this rate, the "20 million yen for old age problem" calculated as of 2019 will be solved from now on.In 30 years, it could become a "40 million yen problem in old ageThat is to say.

Of course, there is no guarantee that a situation like the deflationary Japanese society that lasted for more than 30 years since the late 1990s will not return, in which prices of goods continue to fall rather than rise, so it is not absolutely certain that savings accounts are a bad idea.

in shortEven savings accounts are at risk of having their real value impaired."It is important to know that

Do you really need 20 million yen? Know your own financial requirements

The "20 Million Yen Problem in Old Age" mentioned above is only a model case and is an average amount calculated under the following conditions.

- Husband 65, Wife 60

- Unemployed households

- Assume 30 years of retirement.

- House is owner-occupied (housing expenditures are calculated at 13,656 yen)

- Average salaried household with employee pension recipients

In other words, your income will increase if you continue to work after age 65, if both you and your spouse are working, and if both of you are eligible to receive an employee pension. On the other hand, if you are renting for a long time, your expenses will increase due to rent. Furthermore, if you have been single for a long time, or if you have lost your spouse, there is no point in worrying too much about this model case. The amount of money you really need for your retirement will vary greatly depending on your individual circumstances.

Therefore, you need to create a customized plan to determine how much money you actually need for your retirement and what to do about it.

Below are some rough retirement planning calculations and measures.

Projecting the cost of living in retirement

Prices of stocks and mutual funds rise and fall every moment of every day. Stock prices change not only according to the performance of the company, but also according to social and political conditions, and sometimes they fall sharply in value, resulting in losses.

Check the amount of public pension benefits received.

The risk that a company or country issuing stocks or bonds will default on its debt. Also called default risk. If a company or country goes bankrupt, in the worst case scenario, the entire principal amount may not be returned.

work long hours

Even if stock or bond prices themselves do not fall or even rise, there is still the risk of currency fluctuation if the financial instrument is denominated in a foreign currency. For example, if you purchase a mutual fund denominated in dollars and the dollar rises 101 TP3T after one year, you will gain 101 TP3T in dollars, but if the dollar falls 201 TP3T against the yen (yen appreciation), the price of the mutual fund in yen will fall 101 TP3T.

Increase assets by taking advantage of tax incentives

Market interest rates have a significant impact on bond prices.

- Bond prices fall as interest rates rise

- Bonds issued at existing low interest rates will be less attractive than bonds issued after interest rates rise, so the price of those bonds will fall.

- Bond prices rise as interest rates fall

- When interest rates fall, newly issued bonds are less attractive than bonds issued when existing interest rates are higher, and more people buy bonds issued when existing interest rates are higher. Thus, existing bond prices will rise.

summary

How was it?

It is said that retirement funds are one of the three major expenses in life, along with housing and education. It is very important to consider investing in order to secure funds for retirement, but knowing how to generate funds before starting to invest, knowing the necessary funds (goal), and knowing how to reach the funds (goal) are the first steps to move on to the next step in life with peace of mind.

Comments