The "20 Million Yen for Old Age Issue" from the report submitted by the FSA in 2019 has become quite a hot topic.

Since that time, more and more people seem to be thinking seriously about personal asset formation.

And this year, the "New NISA" system began in 2024. This is a revolutionary system led by the Japanese government called "From Savings to Investment," which guides people's financial assets from savings to investment and encourages asset management.

Many of you may have started investing for the first time this year, or are thinking of starting in the future, as a result of the start of this program.

So today, the new NISA is a good starting point.I would like to pause for a moment to let those who are thinking about "starting to invest" know what asset management is all about.

Let me conclude by saying that there are countless financial instruments in today's society, but the investment with the lowest risk and infinitely large returns is,

Self-investment."

If you were about to close this page thinking, "What, I thought this was information on investment, but it's just self-help and spirituality! If you are thinking, "What's this? If you are thinking, "I thought it was just information on investment, but it's just self-help and mentality! Please read it anyway.

Whether you start investing after knowing the fundamentals of "asset management" and "investment" or start investing without thinking because everyone around you is starting, the world you will see 10 years from now will surely be different.

Continuity is the key to investment. If you start investing casually, you will get scared and withdraw from the market when the crash comes. However, if you start with a proper understanding of investing, you will be able to keep your cool when the market crashes.

I hope that today's column will be of some help to you in building your life plan.

People who should read this article

People who are anxious to start investing

People who are thinking about trying investing for the first time.

People who are just starting to invest and don't know much about it.

People who want to know the basics of investment.

What you need to know before you start investing

Know Asset Management and Investments

The words "asset management" and "investment" are often used together, but actually have different meanings.

What is "asset management?"

It refers to managing assets that you own, such as cash, savings, stocks, mutual funds, and real estate. To manage assets, you must first create assets to invest. There are various options for asset management, including the following types of investment in addition to "investment".

What is "investment"?

It refers to using cash on hand to invest funds in stocks, mutual funds, real estate, etc. to earn a profit. Although the purpose of investment is to make a profit, investment should also be considered a type of asset management. Unlike "speculation" described below, it is an asset management strategy that produces profits slowly while reducing risk by investing over a relatively long period of time.

What is "Savings"?

One type of relatively risk-free (risk-free) investment method is "saving. Strictly speaking, it is not entirely risk-free, but simply depositing cash in a bank is called "saving.

What is "speculation?"

One type of asset management that can be confused with investment is "speculation. Speculation" means buying and selling physical assets such as stocks, FX, and cryptocurrencies in a short period of time, looking at the market to make a profit in a short period of time. Naturally, it involves great risk, and while it can result in large profits, it can also result in large losses. Some data show that 80% of mutual funds managed by professional investors (e.g., institutional investors) lose to index management (a long-term investment approach that aims to achieve results in line with market indices). It must be said that the possibility of amateurs winning is very low due to the high gambling nature of the game.

In today's column, we will discuss "investment," the process of creating funds from which "asset management" is based.

Set investment goals.

Many of you may have become interested in investing in the midst of a drastically changing social climate, such as the pandemic caused by the new coronavirus, anxiety about the future due to rapid inflation (rising prices), increased social insurance premiums and successive tax hikes due to the falling birthrate and aging population, and the introduction of the new NISA system.

Although everyone has his or her own reasons for starting to invest, setting a goal is the most important thing to keep investing and growing one's assets. Just as it is difficult to run a marathon without a goal, asset management without a goal will not last long. You should not start investing because you are worried about the future or because everyone else has started.Decide on an amount that will be your goal for asset building.

For example, it could be a trip abroad next year, or a car purchase in a few years, which are the three biggest expenses in life.home purchase fund, ,Children's Education Fundand ultimatelyretirement money (usu. lump-sum)... I believe that setting short- and long-term goals will motivate you to manage your assets and continue investing.

What are the three major expenses in life?

The three major expenses of life are the amounts that many people target in determining their asset management goals.

The three major expenses in life are housing, education, and retirement.

On the other hand, according to the household survey by the Ministry of Internal Affairs and Communications, the largest expenditure in 2023 for "household income and expenditure of households with two or more workers" was food at 26.51 TP3T, followed by other expenditures including entertainment expenses at 17.21 TP3T and transportation and communication expenses at 16.11 TP3T.

The cost of education is 5.31 TP3T and the cost of housing is 6.01 TP3T.

Then why are "education" and "housing" said to be the three major expenses in life?

This is because, first of all, the above statistical data assumes that the household has an "owner-occupied house. In addition, although "education," "housing," and "retirement" expenses do not account for a large percentage of the monthly household budget, they require a large amount of money to be set aside at a certain time, and these expenses must be prepared systematically.

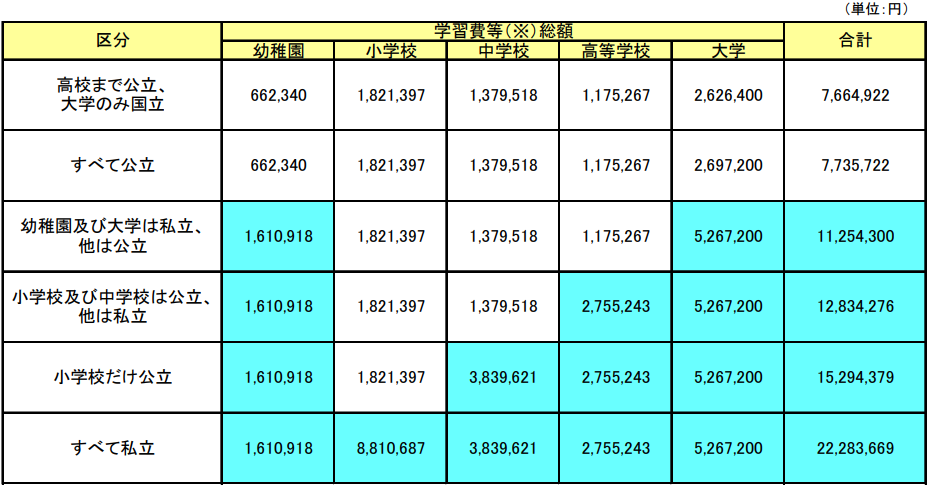

education or school expenses

The average cost of education (excluding boarding and lodging, housing, etc.) for one child from high school to college graduation is approximately 10 million yen even if all of the education is public. If all of them are private, the cost is approximately 23 million yen.

While the lifetime income of a typical Japanese company employee is said to be about 2 million yen in the major metropolitan areas of the Kanto, Tokai, and Kansai regions, the10% (for private school) is the cost of education.

Furthermore, this education cost is from around age 16, when the child starts high school, to age 22, when the child graduates from college.It has to be raised in seven years.The following is a list of the most common problems with the

housing costs (expenses)

Total lifetime housing costs in Japan vary greatly depending on where you live and your lifestyle, but can range from tens of millions of yen to over 100 million yen. The typical cost of purchasing an owner-occupied house in an urban area and paying off the loan is estimated to be in the range of 50 to 80 million yen. On the other hand, lifetime rent if you choose to rent could be about the same or even higher.

If you were to purchase a 60 million yen used condominium in an urban area at the age of 35, at the timing when your child is born and enters elementary school, and if you were to take out a full loan for 35 years until the age of 70, with the recent ultra-low interest rate of 0.341 TP3T, the payment would be as follows. The following is an image of the payment.

- Property price: 60 million yen

- Loan term: 35 years

- Bonus repayment: None

- Borrowing rate: Variable 0.34%

- Initial cost: approximately 1.6 million yen

- Monthly repayment cost: approx. 150,000 yen

- Total repayment amount: 63.7 million yen

The total annual payment will be 1.8 million yen, which is approximately 30% of the average annual income (Tokyo) of 6.12 million yen.

Since the average annual income is pulled down by those with higher annual incomes, the median annual income in Tokyo is approximately 5.72 million yen, and housing costs account for 31.41 TP3T.

Furthermore, this calculation does not include the annual property tax (approximately 100,000 yen), repair cost for a house, and repair reserve fund and management fee for a condominium.

Of lifetime income,Housing costs account for about 321 TP3TThe number of employees is about 1,000.

retirement expenses

Expenses for retirement vary widely depending on lifestyle, area of residence, whether you own or rent, health status, family structure, and other factors. As a general guide, the following factors should be kept in mind.

- Monthly living expenses. according to the 2023 Ministry of Internal Affairs and Communications "Household Budget Survey".

- Monthly living expenses for a two-person household: about 270,000-300,000 yen

- Monthly living expenses for a single household: 150,000-200,000 yen

- Duration of life after retirement at age 65: about 16 years for men and 22 years for women

- The monthly pension amount if the beneficiary starts receiving benefits at age 65:

- In the case of two married couples receiving benefits: approximately ¥200,000 to ¥250,000

- Single recipient: 150,000-180,000 yen

- Actual monthly shortfall after subtracting pension from necessary living expenses

- In the case of two married couples receiving benefits: 50,000-70,000 yen

- If received alone: about 30,000 yen

- After retirement at age 65Total retirement fund shortfall(Calculated over 20 years)

- In the case of two married couples receiving benefits:Approx. 12 to 17 million yen

- In case of single recipient: about 7.2 million yen

This is the figure on which the "20 million yen for retirement" issue is based.

The above Ministry of Internal Affairs and Communications household survey, as mentioned above, sets "housing expenses at 61 TP3T of monthly expenditures, assuming an owner-occupied house." Based on this survey, the monthly shortfall in retirement will be about 16,000 yen for a two-person household, but of course this will not be enough if you live on rent all your life. However, in the case of an owner-occupied house, property taxes will continue to apply for the rest of one's life, and repair expenses will also be necessary.

I would like to talk about this topic again based on my own experience and knowledge as a licensed real estate agent, but in any case, there is no doubt that "retirement expenses" are very important, along with the above-mentioned "education expenses" and "housing expenses. There is no doubt that "retirement expenses" are also very important.

Know how to build your personal wealth.

I understand the problem. Then how do we fund it!"

Asset Management."to begin,Investment."Let's do the following.of, beforeNothing begins without "securing investment funds."

So, before you rush to the bank or brokerage firm with an urgent need to invest, or throw your money away saying, "I can't afford to invest on my current salary! Let's first take a look at the different methods of personal asset building, and what their characteristics are.

- Saving and Household Budgeting

- Monthly review of expenditures

- Organize and review cellular and subscriber services

- Stress is high even though saving money on utilities is not very effective.

- Monthly review of expenditures

- self-investment

- Lowest risk, highest return investment

- Raise salary, change jobs, get a second job, dual job, or start your own business to increase your deposit.

- ordinary bank account

- No risk of loss of principal, no loss of assets due to inflation

- Annual interest rate of about 0.021 TP3T

- term deposit

- No risk of loss of principal, no loss of assets due to inflation

- About 0.2-0.4% per annum interest rate if you are an online bank

- Cancelable at any time, but you may not receive interest if you cancel in the middle of the contract.

- iDeCo (individual defined contribution pension plan) 401K (company defined contribution pension plan)

- Premiums are tax-exempt and tax-preferred

- You can't unload until you're 60.

- Investment is personal responsibility, with risk of loss of principal

- The products available for purchase are selected for their relative safety.

- savings-type insurance product

- In the event of an emergency, they will support your financial obligations.

- Cancellation refund if premiums are paid for a certain period of time, but principal loss if surrendered in a short period of time

- Maturity refund is available when all term payments are completed, and the interest rate is about the same as that of a time deposit.

- High cost for the insurance company's hassles

- individual stock

- high risk/high reward

- Interest rates are unlimited, risk is at worst zero of the invested principal

- investment trust

- Relatively low risk/low return

- Diversified investment without hassle

- Some products have high financial institution fees.

- Expected rate of return depends on the product, risk is up to zero on the entire principal amount invested.

- real estate

- Relatively high risk, high return

- Returns tend to be higher now that borrowing rates are low.

- Ability to borrow against one's own credit and easy leverage

- Low liquidity, sometimes taking a long time to redeem or not redeemable

- If the property is good and individualized, income gain (rental income) and capital gain (profit on sale) can be expected, but if the property is bad, you may be left with only debt even if you sell it.

- commodity

- Financial alternatives such as gold, virtual currencies, FX, etc.

- Gold is relatively low risk, low return, basically the safest asset

- Virtual currency and FX are not investment but speculation (highly gambling)

As described above, there are many ways to "secure investment funds. This isIt is not a matter of picking and choosing; we need to start with what we can, as little as possible.

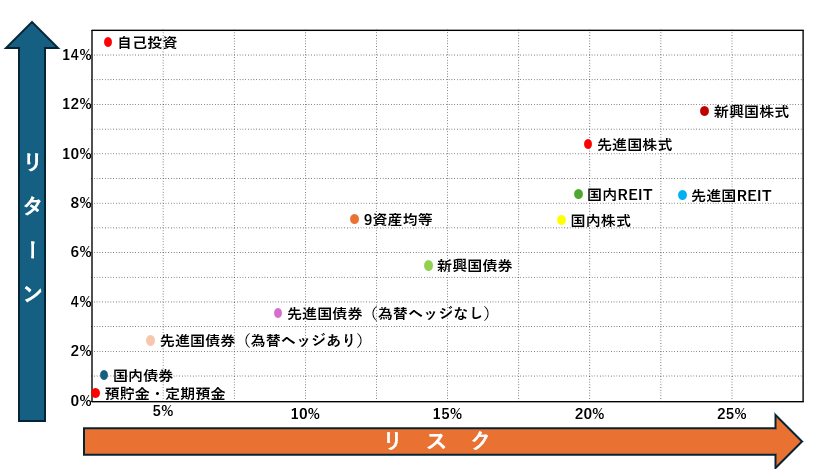

Let's visualize and illustrate the management of investment funds for a moment here.

(Created by the author. This is an image only. Actual investment performance is not guaranteed)

I will discuss the concept and details of return and risk in a later column, but the higher you go on the vertical axis of the table, the greater the expected return (expected profit), but also the higher the risk (horizontal axis, possibility of suffering losses).

You can see that there is almost no return (profit) on a savings account, but at the same time the risk (loss) is extremely low. (Inflation risk also exists in savings accounts.)

Note that there are other factors that are not represented in this table, such as savings, real estate, insurance, and commodities, but these factors are highly individualized and are complicated by other benefits and risks, so it is necessary to consider return and risk for each individual product.

The highest expected return and lowest risk is "self-investment.

The most important thing to emphasize in the above table is,The most low-risk, low-return thing in the world is "self-investmentThat is to say.

However, other than studying, buying a PC to earn extra income on the Internet, buying the latest consumer electronics to generate time for side jobs and study, and exercising for health are also excellent self-investments.

Finally, I would like to summarize the "key elements of investment" in relation to the author's recommended investment method, "self-investment.

- Investing involves risk and return, and while you must accept higher risk to earn higher returns, choosing lower risk will also result in lower returns.

- Risk and return are always a trade-off. There is no no-risk (no risk) high return product (it's a 100% scam!).

- The elements of investment success or failure are time, diversification, and continuity.

- Aim for large profits over a long period of time (at least 5 years, preferably 20 years or more) with low risk (compounding effect)

- Risk can be diversified by incorporating multiple of the above investment factors in a balanced manner (diversification effect)

- In order to maximize the effectiveness of the investment, the "financial power" and "deposit power" that can be invested are the key to success.

- 5,000 profit on an investment of 100,000 yen in a product that yields an annual profit of 5%.

- Profit of 50,000 yen for an investment of 1 million yen and 500,000 yen for an investment of 10 million yen

- Deposit capacity is likely to be enhanced by self-investment.

- Increased salary through studies related to company business.

- Study to earn extra income on the side.

- Qualify to start your own business and earn business income.

- Buy the latest appliances and spend more time studying or working on the side.

- Go to a sports club to stay fit and work forever.

- Improve sales performance by making them look good.

- On the other hand, the risk of losing one's own investment is the cost of books, certification schools, etc., and above all, "time.

- If you study and try for a promotion or certification exam and fail, the knowledge and experience gained from your studies will remain in your head as a benefit. The knowledge in your head is not at risk of being stolen.

summary

How was it?

This is a somewhat lengthy list, but it summarizes what you need to know before you start investing.

Money is very important for life. However,Money is not everything.

The most important thing in life is not money, but how you can live happily as yourself.I think it is a good idea.

We hope that you will find this information useful to help you enjoy each day with peace of mind and with your loved ones and friends without being tied down by money.

Comments